- What is BNPL?

- BNPL statistics

- Tech aspects: integrated shopping apps and credit cards

- Conclusion: Andersen and your IT solution for BNPL products

The ongoing COVID pandemic, global inflation, and overall uncertainty has aggravated the problem of global debt. According to a recent summer report by UBS, the scale of this problem has become truly tremendous. While governments, central banks, and large corporations try to deal with these challenges on their own, individual households and providers of financial services are also trying to shape an answer to this new situation. These attempts have generated a great demand for Buy Now Pay Later (BNPL) products that are rapidly growing in popularity.

So if your eCommerce or finance business needs a new growth spot to win new customers in a competitive environment with enormously high debt ratios, a BNPL payment option delivered within high-performing IT solutions might be the direction to go!

What is BNPL?

Basically, BNPL refers to a finance term, not a tech one. It means short-term lending products enabling clients to buy goods and services now and pay later, at future dates in a specified amount of installments.

Quite often, these credit products are offered on an interest-free basis. However, even if they presuppose some loan rates, they are normally low as long as the client abides by the applicable terms and conditions.

What are the main advantages for a typical consumer, besides increased affordability?

- First of all, this type of lending product is mostly used for online shopping which automatically makes them extremely convenient and easily accessible. In fact, as experts point out, the current situation has given birth to a full-fledged love story between eCommerce retailers and BNPL platforms.

- Second, they do not imply extra fees.

- Third, BNPL products are known for easy approval.

- Finally, these finance products do not affect clients’ credit histories negatively.

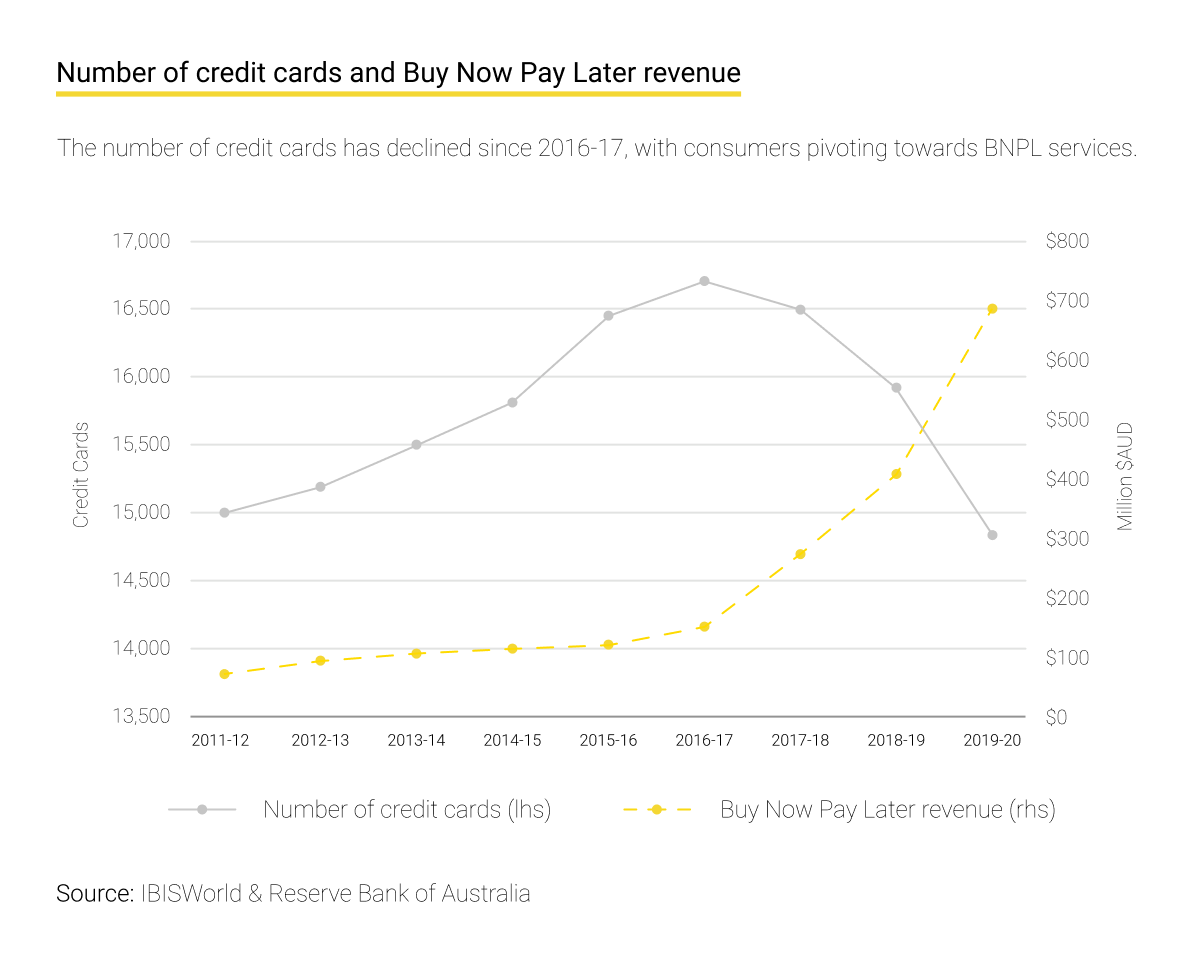

BNPL statistics

As BNPL products are still a relatively new thing, there are not many reliable figures available. The only thing that is clear is that their popularity has skyrocketed recently. Below you can find some interesting data structured by countries, according to Statista.

- Globally, their market share in overall domestic eCommerce payments rose from 0.4% in 2016 to 2.1% in 2020.

- In such a developed country as Sweden this share was as high as 12% in 2016 and 25% in 2019.

- Similar proportions can be observed in Germany with 3% in 2016 and 19% in 2020; in the UK with 1% in 2016 and 5% in 2020; and in Norway with 5% in 2016 and 15% in 2020.

As for the factor of demographics, the following important trend has recently been described by experts. On the one hand, young people are visibly more inclined to use these credit products. For instance, the young British are definitely more likely to become BNPL clients than older consumers. The same holds true for the United States.

At the same time, the growing market demand for BNPL products is not limited to Zoomers and Millennials. Generation X and Baby Boomers have also developed a taste for them. There is a good reason for that!

The C+R research agency published an overview of the advantages that attract users to BNPL programs:

- 45% appreciate the ease of making payments;

- 44% value the increased flexibility;

- 36% like the low interest and 22% are lucky enough to pay no interest;

- 33% vote for the simple approval process;

- Finally, another 33% believe that credit cards are “maxed out.”

Tech aspects: integrated shopping apps and credit cards

Technically speaking, one of the most promising areas to implement a BNPL program is in integrated shopping apps. In the recent overview by McKinsey and Company, the following takeaways from this model are highlighted:

- To be truly effective, such an app should feature an entire range of tech capabilities, encompassing “distinctive merchant underwriting and consumer-fraud models, deep integrations into shopping carts, and sophisticated consumer-service tools.”

- In addition to that, such apps must be engaging enough during the entire buyer journey.

- On top of that, the look-and-feel of such an app should be effective and converting enough to communicate your brand and positioning to appeal to your target audience.

As for other promising approaches, the experts at McKinsey point out card-linked installment offerings and off-card financial solutions. However, if you opt for these schemes, you would still need a proper finance app.

Conclusion: Andersen and your IT solution for BNPL products

BNPL products are a lucrative business nowadays. To benefit from it, one needs to combine finance expertise with a reliable IT solution. If you want to generate more revenue at this intersection of FinTech and eCommerce, contact Andersen for assistance. Over the years, we have implemented dozens of high-profile world-known IT projects in both sectors. As a result, we possess skills, knowledge, and a proven track-record to envision an optimal business flow and well-functioning app!

Among other things, you can familiarize yourself with the solution we delivered for an EU-based company with numerous clients. Everything in it - advanced functionalities, user-friendly look and feel, well-thought-out modules, and bright UI/UX - speaks for itself!